5 Key Trends From KPMG’s Banking Outlook Survey

Focus on the Customer

Banks are refocusing on their customers after several years of prioritizing the regulatory environment as the top concern after the financial crisis, according to KPMG's 2014 Banking Industry Outlook Survey, released this week.

In the survey, 100 senior banking executives were asked to name the top three drivers of business transformation over the next 3-5 years. Changing customer expectations was the most popular choice (cited by 47% of the respondents). The pace of change in technology came in second (43%), and domestic competition came in third (37%). Only 29% chose the regulatory agenda as a driver of business transformation.

The renewed emphasis on the customer is driving banks toward an omnichannel, customer-centric business model, which will drive major change in technology investments over the next few years, KPMG said in its report on the survey.

"In the recent past the regulatory environment has been such a dominant concern… and those pressures still exist, but the survey identifies the fact that executives compliance needs to be normalized," Brian Stephens, KPMG's national sector leader for banking and capital markets, told us. "It needs to be business as usual so they can still spend time on growing the business."

All images come from the KPMG 2014 Banking Industry Outlook Survey.

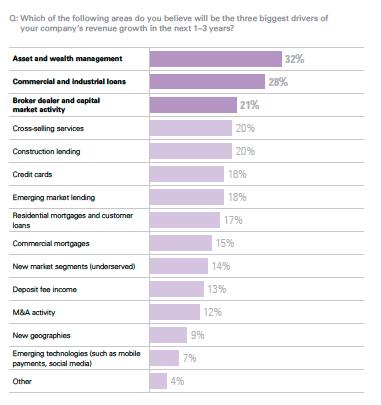

Revenue Growth

As banks look to build their business, they're eyeing wealth management and commercial lending as key areas for revenue growth. When survey participants were asked to pick the three biggest drivers of revenue growth over the next 1-3 years, wealth management was the most favored choice (32%), followed by commercial loans (28%).

Banks have invested heavily in innovation on the retail side of their businesses in recent years, and Stephens expects them to leverage some of that investment to help innovate and deliver new capabilities to commercial and wealth management clients to help drive growth. One area where banks will likely try to leverage their technology gains on the retail side in these other areas is data and analytics.

"With every bank we speak to, data is a top five priority," he said. "Banks recognize that silos and the effect they have on data has slowed their growth and needs to be addressed."

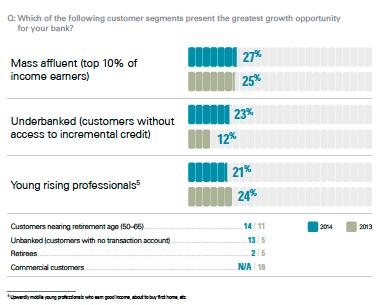

Appeal to the Underbanked

On the retail consumer side, there is increasing interest among banks in attracting and deepening relationships with underbanked customers; 23% of the survey respondents chose them as the customer segment with the highest-growth potential, versus 11% in last year's survey.

The industry's interest in the underbanked is being driven partly by nontraditional financial services providers, like Bluebird, that have made inroads with this segment, Stephens said. Banks can look to attract underbanked customers by delivering faster transactions in areas like bill payment and wire transfers, along with services like debit card management. Many of these customers are students and recent graduates, he said, so banks will have to focus on fee-based services to make them profitable, since they aren't looking for complex loan products yet.

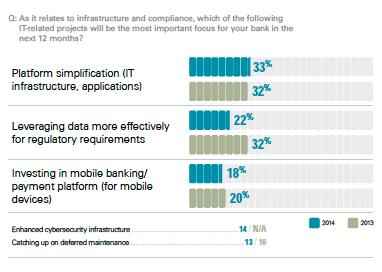

Infrastructure Investment

To build toward a customer-centric model, banks must upgrade and simplify their core IT platforms, and many are prepared to do just that. IT platform simplification was the most frequently cited (33%) major IT infrastructure objective over the next 12 months, followed by making data more effective for compliance (22%) and investing in mobile technologies (18%).

"There's an increasing understanding that this deferral [of upgrading core platforms] has hurt them and can't go on any longer," Stephens said. "It's connected to the strategic business focus, as banks realize that their infrastructure doesn't support a customer-centric, omni-channel approach."

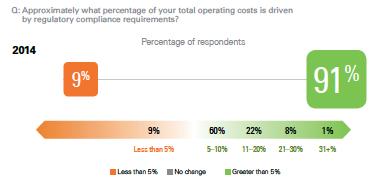

Compliance Still A Big Expense

Even though banks are more focused on growth and satisfying their customers, compliance is still a major issue and a hit to the bottom line. More than 90% of the survey respondents said they are spending at least 5% of their operating budgets on compliance, and 31% said it accounts for more than 10%.

"Time has been helpful in dealing with compliance," Stephens said. "We've been in this new environment for a few years now, and banks have experience with it now… but the regulatory cost piece is still astounding."

Jonathan Camhi has been an associate editor with Bank Systems & Technology since 2012. He previously worked as a freelance journalist in New York City covering politics, health and immigration, and has a master's degree from the City University of New York's Graduate School ... View Full Bio