Evolving US Payments Landscape: Who Wins, the Hare or the Turtle?

The children's tale of the speedy hare and the dependable and plodding turtle is known by many. In a recent webinar, hosts NACHA and The Clearing House provided the latest information on the evolution of the US payments landscape. At the conclusion, one had to wonder if the speedy Clearing House had been outmaneuvered by the dependable NACHA.

In a Dec. 3 webinar, NACHA provided an update on its same-day ACH initiative and announced the issuance of potential rule changes for same-day payments processing. On Dec. 9, it issued a request for comments document with responses due by Feb. 6, 2015.

[For more from WAUSAU's Lawrence Buettner, check out: AFP 2014: Banks Still Determining the Path Forward]

In the same webinar, The Clearing House provided further definition on its decision to develop a real-time payments initiative. Remarkably, the rationale and payment use cases were almost identical to NACHA's.

During the presentation, it was argued that NACHA's same-day ACH and The Clearing House's real-time payment approaches were complimentary to each other. The devil may be in the details.

The distinction between the approaches boils down to timeliness and settlement. NACHA's solution for faster payments lies in two additional processing windows for payments and improved settlement times to address West Coast time zone concerns. The Clearing House's more robust alternative delivers payments immediately to the recipient versus NACHA's same-day availability.

The question that banks and the market will need to sort out is whether same-day is good enough, or whether immediacy matters. With three alternative approaches in discussion -- including the Federal Reserve's payment vision -- it would appear that some rationalization needs to occur on many levels.

- Customer confusion could undermine adoption. Banks will be tasked with developing products to take advantage of the three different approaches. Explaining the different choices to customers will be essential. Pricing may play a major role in making the differences clearer to customers.

- The costs will be high. The Clearing House and the Federal Reserve estimate the costs to the industry at almost $4 billion, with the largest banks requiring investments of $100 million.

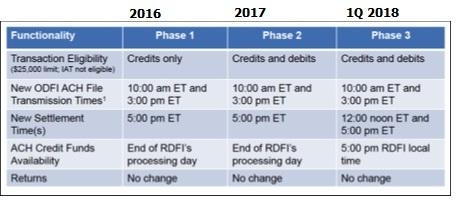

- The investment timeline remains open for two of the approaches. NACHA is proposing a three-year phased approach beginning in 2016. The Clearing House is still finalizing its business case with a potential mid-2016 decision. The Fed is due to provide additional information within the next few weeks.

Though investment will be required, NACHA's envisioned approach uses the current Effective Entry Date field to distinguish from traditionally processed ACH payments and same-day payments. This is far less costly than the $4 billion for real-time payments alternatives advocated by The Clearing House and Fed.

In fact, NACHA predicts that the movement to same-day ACH payments will cost the industry roughly $118 million in technology upgrades and $49 million in new annual operating expenses. To soften the required participation by all banks in the new payment method, the receiving bank (RDFI) will be paid 8.2 cents per transaction by the originating bank (ODFI) to recover the cost of investment.

Rationalizing the three different approaches will be difficult. One constant that must be held firm: The aging US payment infrastructure needs a major overhaul. Though uncertainty remains with the lack of plans and timelines from two of the major players, banks need to begin assessing the potential impact on their current and future product roadmaps. Without putting current plans on ice, investments need to be analyzed for both their short-term return and any potential obsolescence from a new long-term payments vision.

As the race for determining the new US payments landscape has just begun, is it the faster hare or the slower reliable turtle that has the advantage? Or is the Fed the dark horse that will emerge to take the lead? This race is far from over.

Lawrence F. Buettner is a senior vice president at Wausau Financial Systems, which provides receivables technology for financial institutions. He has 30 years of experience in financial treasury management and was a senior vice president at First Chicago. View Full Bio