How the Recent Growth of Auto Lending Is Changing Retail Banking

Credit unions have recovered strongly since the recession. They have experienced record performance in many areas as their membership increases and confidence is regained.

Credit union loan origination hit an annual record of $345.8 billion in 2013, a 4.6% annual rate of growth. Consumer lending led this increase in loan origination, growing at 8.5% year-over-year to reach $189 billion in 2013, while first mortgage loan origination actually fell year-over-year. It should therefore come as no surprise that mortgage tech vendors and others are highly interested in entering non-mortgage consumer lending. With recent declines in mortgage lending and refinancing activity, auto loans in particular are an important and growing segment for credit unions.

The total loan portfolio of credit unions grew 6.9% in 2013. Consumer lending led this loan portfolio growth with both new and used auto loans growing at a faster pace than total loans. New auto sales have surged since 2009, with projections to increase again in 2014. Credit unions held 16 million auto loans at the end of 2013 and held over an 18% share of the total national auto loan market.

[For More On Trends in the Lending Space, Check Out: Social Media And The Next Generation Of Lending Customers]

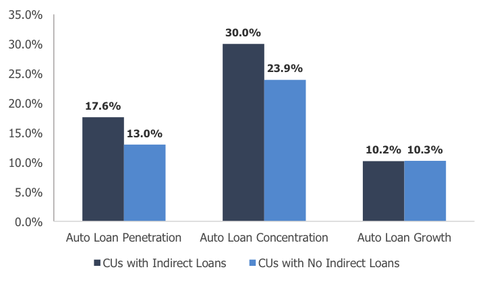

Indirect lending has proven to increase credit unions’ penetration in the auto loan industry. According to data from consulting firm Callahan & Associates and a report from CreditUnions.com, credit unions with indirect loans reported 17.6% in auto loan penetration as of June 2013. This was 4.6% higher than credit unions without indirect loans. Meanwhile, credit unions with indirect loans also posted a higher auto loan concentration of 30%. This was 6.1% higher than those without indirect loans.

Given the recent growth in auto lending, credit unions should be proactive in taking steps to minimize the risk of default. Lending standards are becoming more relaxed, resulting in a rise in loan volumes and creating an environment where potential losses traditionally associated with the mortgage subprime market become more likely. Since holders of auto loans sometimes face additional difficulties in recouping loses, such as more hurdles in repossessing vehicles in high volumes, it is even more imperative that lenders remain proactive in identifying excess risk andpreparing for unexpected defaults. Thus, we are also seeing new opportunities arise along the servicing continuum.

As for drawing a parallel to the housing market, another reason for the increase in indirect lending is related to the relative decline in home prices compared to the pre-recession era. Home equity loans in general are not as readily available as they had been. This has prompted some homeowners to seek alternative financing options that they otherwise might not have considered. As a result, we view the auto and high-end retail consumer lending markets as likely to continue experiencing significant growth.

The heightened level of credit union loan origination and indirect lending activity is changing the market in several ways. First, industry consolidation has created a new imperative for community banks and credit unions to compete with the large, universal banks. Second, the transformation of the retail banking landscape has increased demand in the marketplace for products and services that enable credit unions to automate loan origination and credit decisioning, thereby improving indirect lending programs. At the same time, there is a desire to find new ways to increase loan volume and performance while keeping costs down.

There is a distinct need for technologies that allow credit unions to establish a successful indirect lending program at little upfront cost. This involves enabling access to essential credit data, connecting credit unions with dealers at the point of sale (POS), and automating underwriting guidelines and pricing through an easy to set up and use web-based platform. Perhaps most importantly, indirect lending technologies allow credit unions to compete on a more level playing field with the large financial institutions and captive finance companies.

Other characteristics inherent in successful indirect auto lending solutions include reporting and analysis of loan originators, dealer relationship management, and compliant/audit preparedness. One of the ultimate goals for end-users of indirect lending technologies is to have a complete workflow solution. In terms of barriers-to-entry in the auto lending market, these solutions should integrate with DealerTrack, RouteOne, CU Direct, Open Dealer Exchange, and certain core banking platforms.

Credit unions that put these kinds of solutions in place, and are mindful of the risks in the market, will be well-positioned going forward. Those that fail to do so will continue to be squeezed by increased competition from large banks.

John Guzzo is a Managing Director at Berkery Noyes, specializing in the Financial Technology & Services group. He previously spent eleven years in investment banking and financial services at Giuliani Capital Advisors (formerly Ernst & Young Corporate Finance) and Ernst & ... View Full Bio