Detours on the Road to Digital Banking

Digital is the word of the moment for business in general and in for banking in particular. It's likely to become one of those slippery buzzwords that means whatever the vendor, consultant, or academic wants it to mean. But for now, it effectively describes a mix of online and mobile capabilities focused on customer insight and building on those insights to deliver customized, real-time, and interactive ways of engaging with customers and transacting business across multiple channels.

[Jamie Armistead, senior vice president of digital channels at Bank of the West, argues: Banks Are Not the Yardstick for Digital Customer Experience]

According to new research from McKinsey, there's widespread recognition across all businesses that effective digitization is key to a growing business, and there's an increased commitment of resources to digital work. More than three-quarters of the executives who responded to the McKinsey survey said the strategic intent behind their digital programs is to build competitive advantage in a current business or to create new business and leverage new profit sources. But there's also recognition of organizational and cultural issues, including skills and accountability gaps, that are impeding many businesses from realizing their digital potential. For example, only 7% of respondents said their organizations understand the exact value at stake from digital.

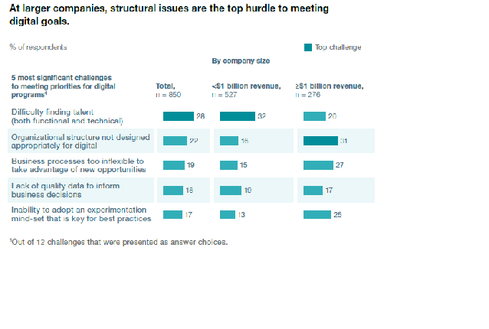

The study, developed by McKinsey specialist Josh Gottlieb and director Paul Willmott, also found that "larger companies" -- those with annual revenue of $1 billion or more -- had particular challenges around organizational structures and business processes that were seen as impeding progress toward digitization. Finding and developing digital talent, especially in analytics, is another concern, particularly for CIOs and CTOs who participated in the study.

These are all pressing issues for banks of all sizes, and it's no surprise that the McKinsey study revealed that the financial services sector is one of the top industries for spending on digital initiatives, including big data and analytics projects.

Fortunately, there is much evidence that banks aren't just talking the talk about becoming digital. They are investing in and committing to digital channels and products. Digital is reshaping the ways banks approach marketing, and it is shaping the concept of customer experience. For example, Capital One's Financial Independence Day Sale is centered on social media. Its #my360 independence sweepstakes encourages consumers to "declare your financial independence" via pictures and posts on FaceBook, Instagram, or Twitter.

Of course, as many of the McKinsey respondents know, digitization cannot be an end in and of itself. Again, it's encouraging that many financial institutions recognize this -- and recognize that digital banking is not primarily about efficiency and cost savings (though those may be among the benefits). It's not like the advent of ATMs 40+ years ago, when many banks thought they could eliminate branches altogether. Banks of all sizes are upgrading their mobile offerings for consumers and corporate customers to improve engagement and retention, improving their abilities to make data-based decisions, and modernizing core systems and infrastructure to support the digital initiatives -- and become more agile and innovative in the process.

"It's an opportune time to link agility and innovation to the major transformation programs that are going on," Jim Reichbach, global banking and securities leader at Deloitte, told me recently. "Banks investing significant sums on large-scale technology programs, be they core systems or [big] data. Billions of dollars being spent on technology. We're asking: 'You're going to replace a financial system, a core system, or you are building a new data system? How do you do it so it's also agile, rather than end up in same place with an infrastructure and ecosystem where everything takes three years and $100 million [to develop]?'"

That might be considered the fundamental question of 21st century banking: How can banks become consistently flexible, adaptive, and innovative while being consistently efficient, productive, secure, compliant, and cost effective, all while serving a constantly evolving mix of constituents (consumers, corporate customers, regulators, employees, partners, etc.)? The answer clearly involves digitization, but no doubt it goes beyond that.

What do you think about the drive to digitization and how it is reshaping the banking industry?

Katherine Burger is Editorial Director of Bank Systems & Technology and Insurance & Technology, members of UBM TechWeb's InformationWeek Financial Services. She assumed leadership of Bank Systems & Technology in 2003 and of Insurance & Technology in 1991. In addition to ... View Full Bio